Team Transitory 2.0

I offered some reflections on Friday’s strong US employment report here.

Until Friday, much of the focus of US inflation had been on commodity price shocks emanating from the closure of the Strait of Hormuz.

These negative supply shocks mostly yielded yawns from Team Transitory 2.0 -- central banks shouldn't respond to these kinds of shocks ("ok, they would acknowledge it if inflation expectations become unmoored").

While the Strait's continued closure remains highly relevant to the US inflation outlook, Friday's NFP data has forced the bond market (and maybe the Fed?) to confront that the US labor market is much stronger than it previously thought.

Some may view the strong upside surprises in US labor market data as fake news/a conspiracy. But honestly, it does seem plausible given:

1) the negative supply shock to the US labor force arising from tighter US immigration policy; and

2) in Q4 2025/Q1 2026 the US policymakers pulled every policy lever as though 2026 was a recession (as opposed to merely approaching mid-term elections) and simultaneously delivered fiscal stimulus, Treasury QE/short WAM/buybacks, monetary stimulus and regulatory stimulus/financial deregulation.

Too much stimulus is not a good thing. Ex- the Strait's closure, it is plausible that the US labor market could have been even hotter.

After NFP, it seems the some are trying to guide that the FOMC can wait until its September meeting to consider a rate hike. Let's see...

the risk of continued inventory draws and parabolic commodity prices does create more recession risk than is currently priced ...

but if the Strait does reopen neatly, the bond market may still have the problem that it appears that US policymakers over-stimulated by pulling all levers simultaneously.

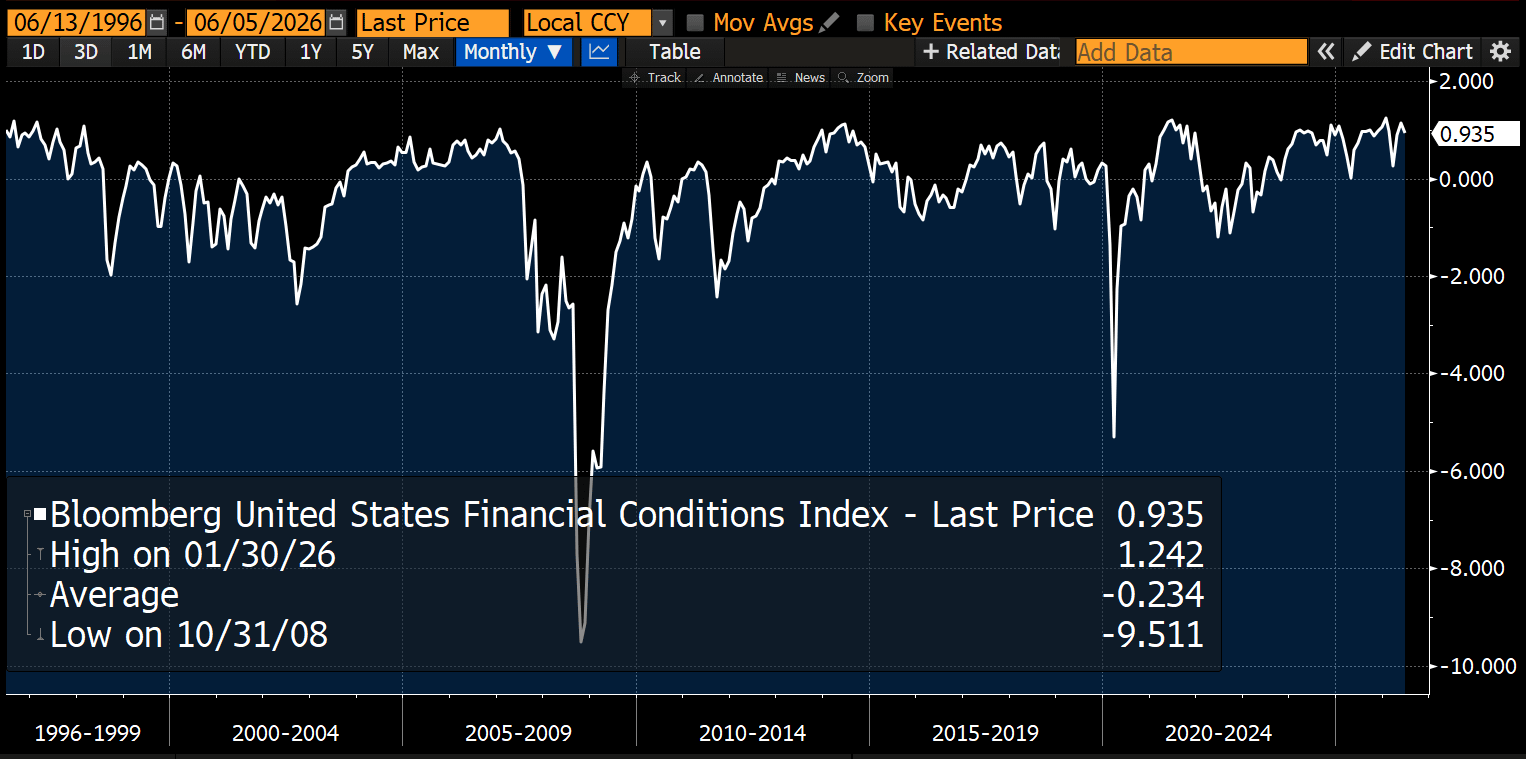

Highly accommodative US financial conditions support this interpretation of excess policy accommodation (Exhibit 1, higher number = easier conditions, most accommodative conditions Jan 2026, just prior to Iran war start).

If the US employment economic surprise sub-index surprises further to the upside (Exhibit 2, positive number indicates greater surprise vs consensus),