Tipping Point -- ‘Detox’ or Stagflation and Recession Risks?

And Don’t Blame This One on the Fed!

In January – well before it was acknowledged by many -- I wrote that it was plausible that US economic growth would weaken, and this wasn't adequately priced in. In my January BTRM column, I noted three channels that could decelerate US growth in 2025:

- fiscal tightening through a shrinkage in the federal spending (workers, contractors, grants) and related economic uncertainty;

-less migration/deportations resulting in both weaker US consumption and labor force growth; and

-rising US economic policy uncertainty, including tariffs, weighing on business fixed investment.

The Bloomberg US economic surprise index (white line) which measures the positive or negative surprise of actual US data releases relative to the consensus economic forecast has moved into negative territory even as the S&P-500 (orange line) has flirted with a correction.

The consensus view was that US economic growth would accelerate after the election and H1 US growth would be stronger than H2. The consensus was wrong on both these counts. Since October 2024, US consensus growth forecasts were revised up by 0.5 percentage points to 2.3% y/y for 2025. The consensus outlook also called for stronger growth in H1 vs H2 2025.

US economic forecasts now are in the process of being revised down. Now many of the same economists/strategists say US data merely suggest a growth slowdown; don’t overly worry about it. My current view is that US stagflation has become more likely than not, with risks of a US recession to follow high because the Fed is likely to wait to act.

Since the start of 2025, we have added more channels weighing on US growth -- specifically, a sharp decline in consumer confidence, falling asset values, a coming procyclical shock to US bank lending and additional negative fiscal impulses.

Consumer sentiment has fallen sharply over the last two months readings. While some may observe that since the 1980s consumer sentiment typically bottoms in the 50-60 range and then equities rebound when sentiment bottoms, it is important to remember that during this historical period there was no stagflation, and the Fed had the flexibility to cut interest rates. In the current circumstance, US consumer sentiment has declined even as US households’ long-run inflation expectations are at 32-year highs, which may reduce the Fed’s ability to proactively cut interest rates.

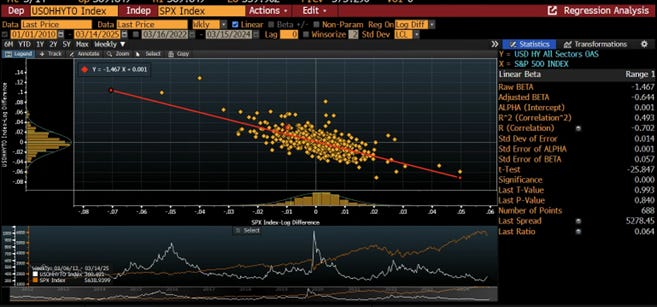

Falling asset values may be expected to negatively impact the consumption of upper income quintiles, reducing GDP. While some may be tempted to view the current equity weakness as a blip, high starting US equity valuations don’t make for “buy the dip.” Peter Oppenheimer, head of global equity research at Goldman Sachs, persuasively discussed in his 2024 book “Any Happy Returns: Structural Changes and Super Cycles in Markets” that history would suggest that 10-year forward returns on US equities are likely to be much lower. A key issue to watch is the performance of high yield US corporate bond spreads which have widened as US equities have declined. Transmission of further US equity market declines into still wider high yield US corporate bond spreads could negatively impact US employment conditions over time. Wages, of course, are corporates’ largest variable cost.

Bank lending is a key engine of credit growth, but most banks have been caught off guard by this US growth slowdown and are likely to behave in a procyclical manner. US bank stocks have fully retraced their post-November election rally (red intervention line), dashing near-term plans for a wave of bank M&A, and risks remain skewed to the downside. The US Treasury curve is flirting with reinversion – this indicator is a common input for smaller banks in assessing economic conditions and setting their risk appetite.

This environment suggests that US banks will pull back from lending because their own market implied default probabilities are rising as the value of their assets become less certain and as slower US economic growth forecasts increase the need for loan loss reserves, reducing earnings. We will have to wait until the next Senior Loan Officer Survey at the end of April to know for certain, but given current conditions it seems plausible that US bank credit growth will also slow. Recall US bank lending is important to small businesses which employ over 50% of the US labor force. Thus, reduced credit availability from banks going forward may help tip the US economy into stagflation and higher US unemployment.

Additionally, while many, including myself, have focused on DOGE’s actions to cut $1.8 trillion in discretionary spending, fiscal policy is also affected through US government tax expenditures. Such income tax breaks collectively total $1.6 trillion. The Biden Administration’s Inflation Reduction Act (IRA) approved $270 billion in tax credits/tax expenditures. While IRA legislation remains in place, in January the Trump Administration signaled that it may utilize impoundment to withhold Inflation Reduction Act (IRA) tax credits. While the use of impoundment may or may not withstand subsequent legal challenges, based on some recent discussions, the uncertainty around the status of the IRA tax credits seems to be having a negative effect on continued tax expenditure related IRA spending/fiscal stimulus. Like DOGE, the impact is difficult to quantify from available data, but is another negative fiscal impulse. Note that I welcome suggestions from readers on where to find current IRA tax expenditure data but I think it is published with such a lag that we will only know in hindsight.

These additional four channels (declining consumer confidence, falling asset values, procyclical bank lending behavior and additional negative fiscal impulses related to IRA tax expenditures) increase the likelihood of below trend US economic growth and rising unemployment.

I got some pushback recently for pointing out the sharp decline in the Atlanta Fed GDPNow which suggests that the US may have already entered recession.

The question of the treatment of gold imports in the Atlanta Fed’s model remains unresolved even as some large bank economics teams have stated that the Atlanta Fed does not need to subtract these gold imports because these gold purchases were monetary in nature. Even after reading this piece from the Atlanta Fed and another piece in the FT, it still seems unclear whether the imported gold was or was not captured in “C.” For example, if a retail investor in gold walked into a jewelry store and bought gold coins or bullion made from imported gold – I think that purchase would be captured in “C” and thus, the import of the gold “M” should be subtracted from US GDP. It seems like this fundamental question remains unanswered. On a related note, if a person walked into a jewelry store and bought a 22k gold bracelet that was made with imported gold and had the same economic motivation for the purchase as buying gold bullion, should it be treated as consumption or a monetary transaction? What about Americans’ online Costco gold purchases – are they included in “C”? I bet they are.

At the same time, inflation remains above the Fed’s target and inflation risks remain elevated. Long run inflation expectations already are near levels seen during the 1990 Gulf War. The most recent CPI release shows super core inflation coming down, but still running at 3.78% y/y NSA as of end February. One year inflation swaps (yellow) have risen from 2.33% prior to the November election to 2.93% in March, reflecting the inflation derivatives market’s concerns about tariffs’ potential impact on near term inflation even as 5yr 5yr forward inflation swaps (red) reflect much lower inflation expectations, consistent with the realization of downsides for US economic growth after an initial inflation shock.

Thus, US economic stagflation seems more likely than not in 2025, with risks that this environment devolves into a US recession because Fed easing arrives late (or we may already be there). For this week’s Fed meeting, I expect a pause in the Fed’s balance sheet run-off, as noted in last month’s column. It is probably best that the semi-public debate between Dallas Fed President Logan and SOMA manager Perli be resolved with a QT pause. A pause to QT would demonstrate a good “reading of the markets” that stagflation risks are rising and the benefits of bringing banking system reserve balances down incrementally is not worth the incremental risk as macrofinancial fragility is rising. The January FOMC minutes have created some expectations in markets of a possible QT pause. Failure to deliver that could lead to a tightening US financial conditions at the wrong moment. Upward revision to inflation forecasts in the Summary of Economic Projections would not be surprising. Markets are currently pricing in a first Fed rate cut in July which is probably about the latest we get Fed rate cuts.

Trump Administration “Detox Plan”

In my February column, I noted that “the Administration repeatedly has spoken about the willingness to ‘impose hardship’ or ‘pain’ – but, just like tariffs, financial markets seem unable to take these things seriously until it is wildly self-evident.” Indeed!

In early 2025, the market focused on potential positives about the Administration’s economic agenda –deregulation and tax cuts – and ignored negatives like tariffs and the Administration’s pursuit of deep changes to the global monetary and geopolitical order. Perhaps part of the challenge for the US economic consensus also is that they did not appreciate that the rapid Q1 2025 shift in the US economy could be by design, not by accident.

Both President Trump and Treasury Secretary Bessent repeatedly have spoken about about “hardship,” “pain” and even “some detox.” We don’t really know the full details of “the detox plan” because the Administration does not seem to view it as necessary to explain its economic and related geopolitical policy agenda to the public. This lack of more fulsome explanation of policy is unfortunate. Leadership is about articulating a clear vision and accountability for that vision. The absence of clear and effective communication understandably erodes public trust in policymaking. Trust is foundational to finance (and other things too!) and has begun to dissipate.

In the absence of a clear explanation of “the detox plan,” let me try to offer a rough in-paradigm interpretation. The Administration appears guided by several core ideas:

1) China poses a significant military threat and the US is paying too much for its allies’ security;

2) the US needs to reindustrialize and reduce its trade deficit which it views as having reduced US competitiveness;

3) US government debt/GDP is nearing a tipping point and the situation must be stabilized.

4) Creating a US sphere of influence that is self-sufficient is both desirable from a national security perspective and over time disinflationary.

Given this set of concerns, one might develop economic policies along the following lines. Engineering a growth slowdown related to downsizing fiscal spending and tariffs might help reduce trade imbalances. Associated declines in US financial markets may help soften demand from high income quintiles who have benefited from asset appreciation. Weaker US economic growth may encourage the Federal Reserve to significantly lower interest rates which further reduces the budget deficit and also facilitates terming out the Treasury market. A growth slowdown might also be used to encourage Congress to enact legislation to end Fannie Mae and Freddie Mac’s conservatorship and transition away from an implicit government guarantee and remove the federal tax exemption for municipal bonds -- a tax cut pay-for -- which also may increase demand for Treasuries. A lower US budget deficit can help justify significant tax cuts in H2 2025 – including the rumored elimination of all taxes on income up to $150,000 -- to support the economy and soften the blow of “plan detox.” Faced with tariffs, US trading partners might agree to spend more on defense and to help fund US reindustrialization. Weaker consumption and growth may give time for US domestic industry to adjust. Weaker growth and lower interest rates imply a weaker dollar which also may support a rebalancing of US trade.

A careful reader might notice a lot of “mays” and “mights” in the paragraph above. I don’t know this 100% to be the policy approach, but such an economic strategy – assuming I am in the ballpark with its broad contours – could address the Administration’s stated long-run objectives.

What are some economic policy tensions/contradictions in this strategy?: